We live in a world which is today dominated by the unending and increasingly violent cycles of economic booms followed by their subsequent busts. These continuous gyrations from boom to bust and back again to boom are in fact mere artifacts of the artificial manipulation of the money supply propagated through the intervention in credit markets by central banks. Specifically, the “boom” is accompanied by a prolonged period of excessively low-interest rates which incentivizes borrowing for inefficient and sub-optimal use, while the “bust” is triggered by a decrease in money supply growth which subsequently serves to expose all of the prior errors of the boom years.

The theory behind this boom-bust cycle was explained in a previous article (see Forecasting the Boom-Bust Cycle), in which it was shown that peaks and troughs in economic growth are typically preceded by peaks and troughs in the money supply. This relationship allows for the money supply to serve as a forewarning against impending economic downturns as early as 3 years in advance of an actual slowdown in GDP growth. What the previous article and its accompanying chart does not explicitly illustrate, however, is that each significant contraction in money supply growth has throughout history been the trigger for some type of negative economic “event”. Much more so than merely signaling a decrease in economic growth, a sharp decline in money supply growth serves to expose the reckless investments and speculations made during the boom years, typically involving the purchase by both businesses and individuals of high-risk and highly-leveraged assets.

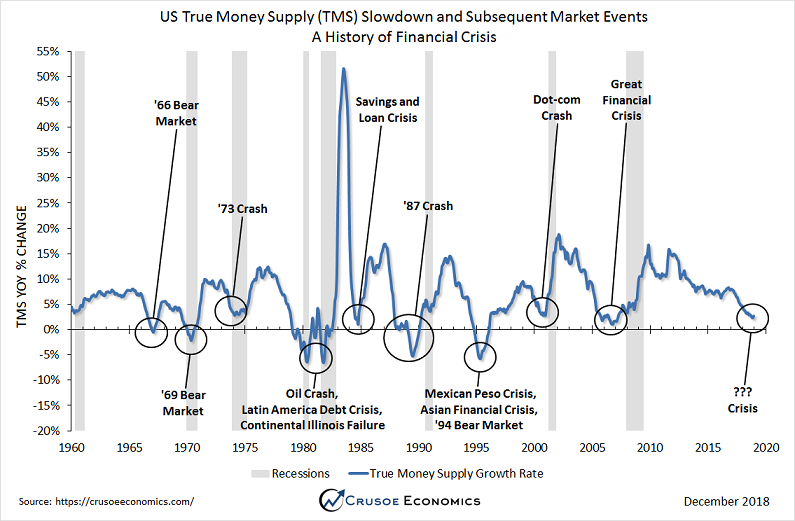

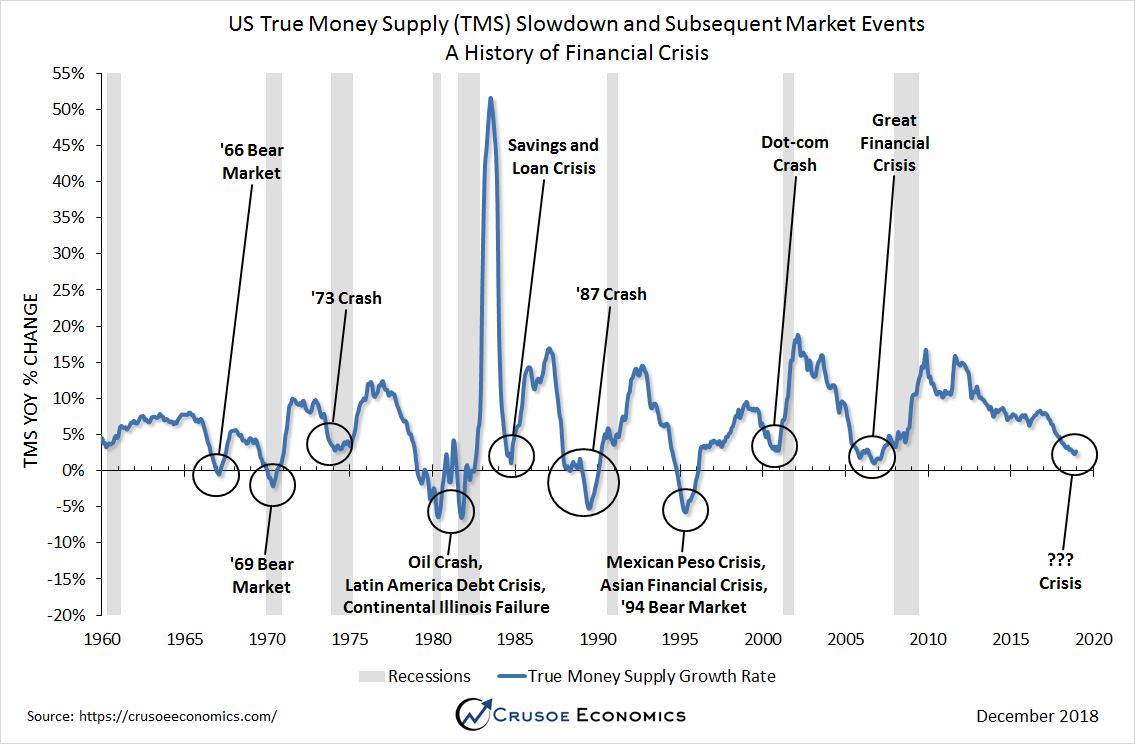

The leveraged nature and scale of the mal-investment made during the boom years has historically led to some type of financial market crash, panic, crisis, or other global sell-off when liquidity is at last withdrawn alongside the artificial demand emboldened by the prior increase in the money supply. The chart below* makes this relationship abundantly clear.

{kind=link}

Illustrated above are the various historical financial “events” from 1960-2018 shown alongside the rate of change of the money supply as measured by the “True Money Supply” (for details on the True Money Supply (TMS) measurement, see Follow the Money Supply). It is clear from the graph above that each significant crisis event was precipitated by a fall in the money supply which in turn was precipitated by a tightening of central bank policy through a raising of interest rates. There is perhaps no more obvious illustration that the boom-bust cycle of today is in fact caused by a tightening of central bank policy, as every single recession in the near-60 year history above was in fact preceded by a decline in the growth rate of the money supply.

While the chart above highlights the absolute troughs in money supply growth, it is important to note that the “trigger” for each crisis was a reduction in the money supply growth rate below some critical threshold on the way to each low, not the absolute low itself. Due to the time lag between each negative economic event and the preceding decrease in TMS growth, the exact threshold which caused each specific event cannot be known either in advance or even in retrospect.

In many cases the trigger for each financial crises is obvious, such as with the Great Financial Crisis of 2008 or the Dot-Com crash of 2001. In other cases, however, it is far less obvious. The Savings and Loan Crisis illustrated above, for example, actually stemmed from the tightening of liquidity in the late 1970’s, and might have been classified as an “event” triggered by the decline in TMS growth from the late 1970’s to early 1980’s. However, government deregulation meant to prop-up Savings and Loan institutions in the early 1980’s led to even further reckless behavior and rash lending, delaying the liquidation event even further still until 1986 following a tightening of monetary policy by the Federal Reserve through a raising of the interest rate.

As another example, while the TMS weakness in the early 1990’s caused a minor equity bear market in the United States in 1994, it had larger repercussions on many developing countries which had previously maintained a currency peg against the US dollar. As the Fed began tightening monetary policy and raising interest rates in the early 1990’s, it had the effect of strengthening the US dollar in foreign exchange markets, causing countries that had pegged their currencies to the US dollar to appreciate their currencies as a direct result. The tightening of liquidity in the US thus had unintended spill-over effects to Mexico and other countries in Asia as it served to negatively impact the cost of exports in world markets. US monetary policy thus served to contract liquidity globally which consequently triggered the Mexican Peso Crisis of 1994 and the Asian Financial Crisis of 1997 a few years later, although weakness in many Asian countries could be seen as early as 1996.

The record of financial crises perpetuated by the unending boom-bust cycles of modern-day times is thus a long and varied history that is both unrelenting in its repeatability yet at the same time unpredictable in breadth. With money supply growth currently approaching what looks to be a secular low, the only question at this late stage in the game is exactly what shape and form the next great financial “event” will come to embody, and exactly how widespread and far-reaching the coming crisis is ultimately likely to be.

(*) The chart in this article was inspired by the fine work of Jeffrey Peshut over at RealForecasts.com. Jeffrey produces his charts based on True Money Supply metrics supplied by Michael Pollaro, while I have independently calculated the True Money Supply from publicly available Federal Reserve data.