Because investing is ultimately the practice of making reasonable tradeoffs between risk and return, having an accurate measure of both is a critical component of effective asset allocation. Returns, of course, are a simple enough thing to measure – they’re merely your portfolio’s compound annual growth rate over time. Trying to determine an objective measure of risk, on the other hand, is where things begin to get a great deal more complicated. This isn’t to say that the investment industry has yet to settle on their preferred definition of risk – they simply use an investment’s volatility. Unfortunately, the vast majority of real-world investors experience risk in ways which aren’t realistically captured through popular volatility metrics commonly used in modern finance. Investors don’t care about volatility, per se. What they care about are losses.

Why Volatility isn’t Risk

Now to many people volatility and the risk of losing money are one and the same thing. After all, the popular measure of volatility – standard deviation – is simply the variability of returns around an average. So if an investment occasionally produces an annual return 15% above or below its average, is this not inherently riskier than once which occasionally produces returns 5% above or below its average? The answer to that question is no, and for two reasons. In the first place, standard deviation measures both upside volatility and downside volatility, but no investor in their right mind thinks of upside volatility as risk. An investment that doubles over a short period of time is certainly highly volatile, but investors don’t perceive sudden outsized returns as something to be avoided – they perceive them as profits.

The second and far more significant issue with standard deviation is that, as a statistical measure, it is completely path-independent. This is to say that while standard deviation is meant to measure the degree of dispersion between returns, it fails to factor in the sequence that those returns occur in real life. This was a phenomenon depicted beautifully by Peter Martin, author of “The Investor’s Guide to Fidelity Funds”, which is updated and reproduced below1.

The chart above shows 3 investments, each with identical returns and identical standard deviations. The actual performance of the S&P 500 from 2000-2009 is overlaid with a simple re-sequencing of investment return data to create both a “flattened” curve (designed to reduce drawdown depth and duration) and a “sorted” curve (which simply sorts returns from lowest to highest). By altering the order by which returns occur over time, investors receive the same return with the same volatility, yet with vastly different real-world levels of risk. Investors putting their money into the “sorted” investment based on its historical standard deviation would surely be in for a rude awakening relative to an investment in either the actual S&P500 and the “flattened” curve scenario depicted above.

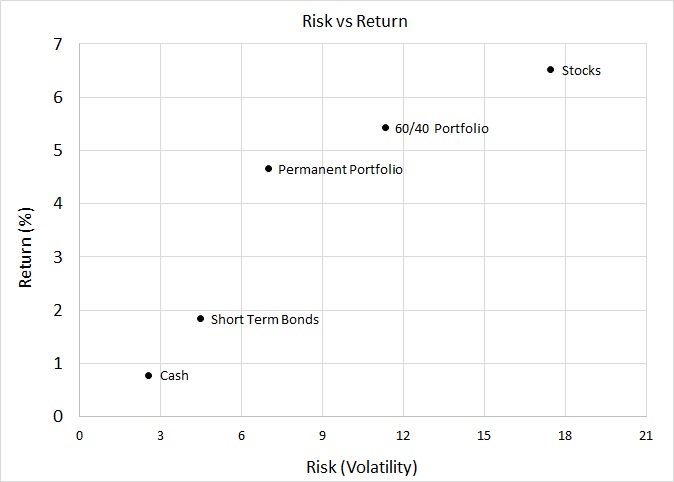

Of course, this is hardly the only peculiarity that appears when examining the assumption that volatility and risk are one and the same thing. Below is the standard industry risk/return depiction for several investments, illustrating how certain portfolios can indeed increase returns, but usually at the expense of added risk. In keeping with current industry-preferred statistical measures of risk, the horizontal x-axis in the chart below uses standard deviation as its proxy for investment risk.

Surprisingly, the Permanent Portfolio, which holds an equal allocation of stocks, bonds, gold, and cash, is depicted as being a far riskier investment than one would assume. For the uninitiated, the Permanent Portfolio was designed as a stable “all-weather” portfolio designed to minimize drawdowns in any economic environment. Extensive back-testing of this portfolio has indeed confirmed that the Permanent Portfolio loses money fairly infrequently, and when it does lose money, it tends to have rather shallow drawdowns which are extremely quick to recover. Risk-averse investors are typically attracted to this asset allocation because it protects from portfolio drawdowns exceedingly well. Measuring risk using volatility, as the above chart does, would seem to fail this very basic smell-test.

Cash, of course, is depicted in the above chart as being extremely safe, as its principal value tends to fluctuate very slowly in any given year, even once inflation is accounted for. This likely corresponds with how many investors tend to think about cash, but these investors forget that inflation risk over any lengthy period of time is no less potent than the risk of capital losses. The 1970’s and early 1980’s were a period of considerable inflation during which US cash investors incurred considerable real losses on their savings accounts. During this period, in inflation-adjusted terms, cash suffered a peak-to-trough drawdown of approximately 12% and delivered real losses to cash investors for a period of 10 consecutive years. While cash may have certainly incurred these losses in a non-volatile way, no real-world investor would consider losses of such magnitude and duration to be “low-risk”.

To illustrate this point further, the following chart shows the relationship of cash and equities with respect to capital loss risk and inflation risk.

As shown above, stocks are depicted as being the asset that maximizes capital loss risk, which is entirely consistent with the risk/return graph denoting equities as the highest-risk asset class. Cash, on the other hand, has a near-zero risk of capital losses in nominal terms, but generally finds itself over-exposed to considerable inflation risk over time. Thus, given that cash is the asset that has traditionally served to minimize capital loss risk at the expense of maximizing inflation risk, it would appear that denoting cash as being a near-riskless asset is incoherent with its historical record. Indeed, if inflation has historically been a significant risk factor for a pure cash portfolio, then one can only conclude that volatility is simply an inadequate measure of real-world risk.

Risk and the Real World

While risk tends to mean different things to different people, one thing about human nature that never changes is that people hate to lose money. Approaching the concept of risk with the pure goal of loss minimization in mind, a far more reasonable definition of risk than simple volatility would be the likelihood of incurring losses. This approach, of course, is hardly novel. Many investors attempt to measure the frequency of drawdowns as a better benchmark of risk, while others resort to magnitude of losses or “time to break even” following a market drawdown. Indeed, many people who dismiss volatility as a measure of “riskiness” tend to use one or more of these metrics as their preferred measure of investment risk. Graphically, these three properties are depicted in the chart below.

The above chart is meant to illustrate a better framework for risk that more closely aligns with how investors actually perceive risk in the real world. This is a risk that is raw, palpable, and highly visceral to an investor who may have just witnessed a good portion of their life savings evaporate into thin air. Investors ultimately want an investment that loses money infrequently and, when it does lose money, does so only in small amounts, and even then only for short periods of time. An investment that experiences reasonably steep losses in a short period of time is of course risky, but if the investment tends to recover relatively quickly, is it necessarily riskier than an investment that incurs smaller successive drawdowns over a much longer period of time? The answer isn’t clear-cut, but at a bare minimum, the factors that would need to be included in any statistical measure of real-world investment risk would seem to include:

1. Frequency of drawdown

2. Depth of drawdown

3. Duration of drawdown

One of the best ways to depict this type of risk is simply by showing the historical drawdowns of various asset classes from their most recent all-time highs. The chart below depicts all such inflation-adjusted drawdown periods from 1972 to 2020 for cash, stocks, the 60/40 portfolio, and the Permanent Portfolio. Any drawdown of 0% means that the investment in question has achieved a new all-time high for the year, while any value less than 0% denotes the drawdown from the most recent all-time high. For example, the 60/40 portfolio reached an all-time high in 1971, but by 1974 was approximately 37% below the 1971 high. It was not until 1983 that the 60/40 portfolio managed to exceed its previous 1971 peak.

The chart above provides an unfiltered visualization of the most important measures of risk that investors likely care about, illustrating the frequency that an investor can be expected to lose money, the magnitude of the drawdowns, and the time to break even. It should come as little surprise that both the 60/40 portfolio and the 100% stock portfolio have historically delivered stomach-churning losses rather frequently. Nor should it come as a great surprise that the Permanent Portfolio has shown incredible resilience, experiencing a significant loss on only a single occasion while still managing to reach new highs only a year later.

What also should come as little surprise, but will still prove enlightening to many investors, is how risky cash has historically been on an inflation-adjusted basis. While it has never experienced a large-scale loss in any single year, it historically incurs frequent small and sequential losses which, taken together, tend to add up to extremely lengthy drawdowns of substantial size. Indeed, cash is currently in the midst of a 12-year drawdown period from its inflation-adjusted peak in 2008. Measured against this peak, an investor with 100% of their portfolio in cash is currently underwater by approximately 14% once inflation is taken into account. Looking again at the different drawdown profiles in this new light, it becomes far more difficult to make the argument that cash has the lowest overall risk among the four different investments depicted above.

A “Total Risk” Framework

In attempting to find a more realistic proxy for risk, our aim should be to aggregate these three essential properties of risk (drawdown frequency, depth, and duration) into a single metric against which true investment risk can be measured. While it is true that no statistical measure can ever truly capture how investors actually perceive risk, it would undoubtedly be head-and-shoulders above the current widely-used alternative of standard deviation. Fortunately, it isn’t necessary to devise a completely new metric that aggregates real-world investment risk into a single number – it turns out that one already exists.

The Ulcer Index (UI) is a statistical measure of risk invented by Peter Martin and first published in 1989 in the book The Investor’s Guide to Fidelity Funds by Peter Martin and Byron McCann2. It was devised as an alternative to standard deviation and as a means to more accurately capture the types of risk that real-world investors actually care about – losses. Performing a deep dive into the formula behind the UI shows that it is indeed sensitive to all of the properties of risk identified above – drawdown frequency, drawdown depth, and drawdown duration. The greater the value of the Ulcer Index, the riskier the portfolio, with a UI value of zero indicating an investment with a history of precisely zero losses.

A detailed analysis of the exact formula used to calculate the UI is beyond the scope of this article, although the precise details are available on Peter Martin’s website for those who wish to learn more1. For all intents and purposes, though, the UI encapsulates an investment’s overall “total risk” rather eloquently, and certainly does a far better job at passing our basic “smell test” than standard deviation. Using this new measure of total risk, we can now plot an updated version of the classic risk/return chart using the UI as a proxy for risk instead of volatility.

Using this new framework for measuring risk, the reader will immediately notice that cash no longer holds the crown as the de facto riskless asset. This intuitively makes sense once an investor comes to the realization that cash, rather incredibly, has spent more time in a state of drawdown than it has outside of it. Indeed, in addition to suffering drawdowns that are both frequent and long, these relatively small successive losses incurred by cash-holders have in reality culminated in substantial total drawdowns which few investors would realistically classify as “low-risk”.

But if a 100% cash portfolio is no longer the minimum-risk investment according to more realistic measures of total risk, then which investment is? It’s clear from the previous chart that the Permanent Portfolio is an incredibly safe investment with a lower overall risk level than cash, but is it really the portfolio with the minimum total risk among all other possible portfolios? It’s hard to say for sure, but in an attempt to find an asset allocation with a lower level of risk than the Permanent Portfolio, the Ulcer Index was analyzed for 20 different popular investment portfolios, in addition to all the major asset classes. While some portfolios came within spitting distance of the Permanent Portfolio, none had a lower total risk, making the Permanent Portfolio our candidate for the most efficient loss-minimizing statically allocated portfolio available to average investors.

None of this should be particularly surprising, of course, as the Permanent Portfolio was specifically designed with the primary goal of maximizing safety throughout any economic environment. The fact that our preferred measure of total risk captures this fact is simply confirmation that the overall risk of an investment isn’t measured by volatility – it’s measured by losses. All of this isn’t to say that investors who hold a large portion of their portfolio in cash don’t have entirely sensible reasons for doing so, even if they’re likely exposing themselves to considerably more risk than they probably realize. For while cash has a higher level of total risk than many investors assume, it nevertheless has the one property that remains unmatched by virtually any other asset class – the unique property of immediate liquidity.

Cash, after all, tends to accrue losses slowly over time, with the probability of large-scale drawdowns on any given day typically being quite small. While we have seen that cash is a relatively risky asset overall due to inflation, it nevertheless minimizes the likelihood of experiencing large drawdowns in the very short term. Within the time-span of a year or, perhaps, even several years, investors are often more willing to stomach a near-guaranteed loss of a few percent versus a much smaller chance of losing, say, 15 percent. Over time, however, these minor successive drawdowns tend to balloon in size dramatically, growing from merely small annoyances into large and unrecoverable losses. Holding cash over long periods of time is thus truly the embodiment of the term “death by a thousand cuts”.

Concluding Thoughts

While standard deviation is certainly a useful metric worth knowing in and of itself, using a total-risk approach instead of a volatility-based approach offers investors a much more realistic framework for effectively managing real-world risk. Rather than simply treating cash as the default riskless investment, we instead begin with the general assumption that the Permanent Portfolio serves as the new de facto “safe” investment based on our total risk framework. Despite the fact that many investors continue to believe in the “safe-haven” status of cash, in terms of drawdown depth, duration, and frequency, the Permanent Portfolio has comparatively been a far safer investment on a historical basis.

Today’s investors are accustomed to mixing risky assets with less risky assets when constructing target asset allocations as they attempt to balance their desired return with their personal threshold for pain (ie. risk). Cash, as the widely-perceived riskless asset, is typically only granted a minimal allocation in such portfolios, as its risk-reduction properties go hand-in-hand with a rather large drop-off in return. This is usually why we often see risky assets such as equities mixed with assets like bonds, which are generally considered riskier than cash, but without the accompanying large reduction in returns. The Permanent Portfolio, conversely, is a rather curious asset allocation. In addition to being the least risky asset allocation in our analysis, it also offers returns far in excess of both cash and bonds. As such, from a returns point of view, it offers a far superior starting point for constructing a properly balanced and structurally diversified low-risk portfolio.

One of the insights of Modern Portfolio Theory is that by adding risky assets to safe assets investors can often, rather counterintuitively, both reduce risk and increase returns simultaneously. The obvious next step is therefore to blend the Permanent Portfolio with other higher risk assets to see if we can uncover an alternative asset allocation with an even safer risk profile. Of course, using the Permanent Portfolio as our min-risk investment, it would also be beneficial to begin introducing other asset classes into the mix to see what insights, if any, we can glean through the new lens of our “total-risk” approach. After all, an investment framework that uses investment losses instead of volatility as its barometer for risk is likely to reach a far different conclusion regarding the risk-return tradeoff for diversified investors. This analysis will be the focus of a future article.

1 https://www.tangotools.com/ui/ui.htm

2 This book is out of print, but an online version exists at http://www.tangotools.com/ui/fkbook.pdf