With growing weakness in the Canadian real estate market becoming more evident with each passing day, there has been no lack of speculation that the recent decision by the Bank of Canada (BoC) to begin purchasing Canadian Mortgage Bonds (CMBs) is merely laying the groundwork for some form of future “QE” in response to a potential collapse of the residential real estate market in Canada. Many analysts point to the asset monetization supposedly undertaken by the BoC in response to the 2008 financial crisis as an indication that a similar operation will be undertaken in response to deteriorating liquidity and solvency conditions among Canadian banks in the event of another severe real estate contraction – a contraction which many pundits believe will be far worse than the one experienced in 2008.

But exactly how valid is it to claim that QE was undertaken by the BoC during the 2008 financial crisis and how likely is it that they will engage in QE again this time around? Furthermore, if indeed the BoC once again turns to these types of emergency liquidity measures to prop up the residential real estate market and by extension the entire Canadian financial system, in what form can we expect asset monetization to unfold in the future given the events of the recent past? This article is the first part of a two-part series meant to examines the past, present, and future state of QE in Canada in an attempt to answer these fundamental questions.

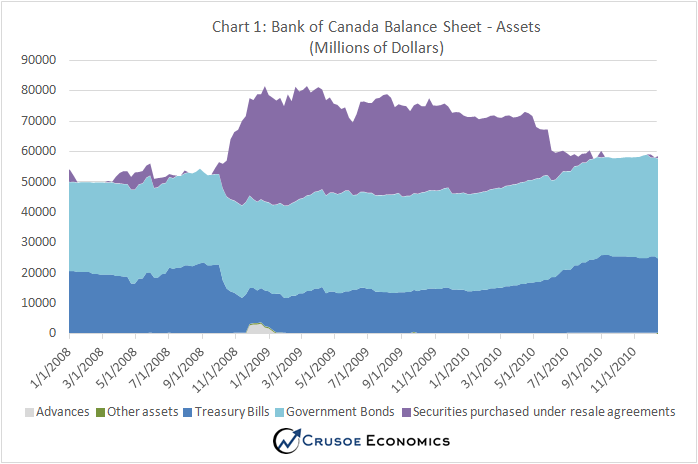

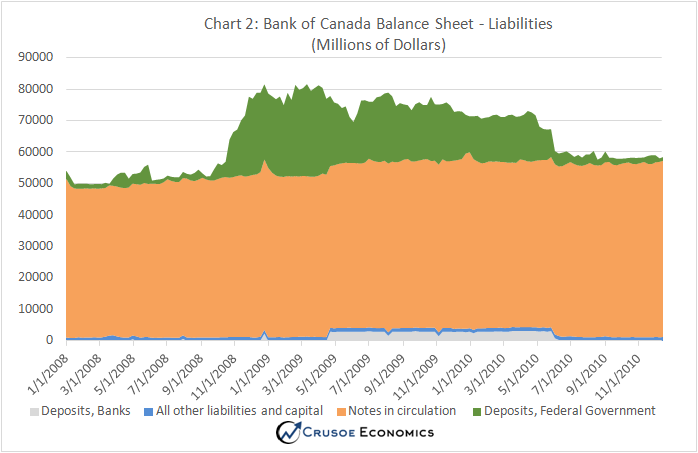

We begin the analysis by first taking a closer look at how events unfolded during the 2008 financial crisis and examining the oft-made claim that QE was aggressively pursued by the BoC through asset purchases of Canada Mortgage bonds, private corporate debt securities and various other forms of Federal and Provincial government bonds. Chart 1 below shows the asset side of the BoC balance sheet over the course of the 2008 financial crisis, and Chart 2 shows its liabilities.

When the financial crises hit in 2008, we can see clearly from Chart 1 that the BoC did indeed engage in large-scale asset purchases of various government, mortgage, and private sector debt securities in record-breaking quantities, which is reflected in the huge spike in “Securities Purchased Under Resale Agreement” (the purple area in Chart 1 which began to spike in October 2008). Now when the BoC purchases securities in this manner from commercial banks, it pays for these bonds with newly-created money, crediting the accounts the commercial banks hold at the BoC with something called “settlement balances”, also known as “reserves”. The end result of this money-creation process would therefore normally be reflected as a corresponding increase in “Bank Deposits” on the chart of BoC liabilities (the grey area on Chart 2). Instead, what we see is a huge spike in “Federal Government Deposits” (the green area on Chart 2), which is simply deposit money of the Federal Government held in its account at the Bank of Canada. But how, we are left to wonder, did reserves injected by the BoC into the banking system suddenly become “Federal Government Deposits” held at the BoC?

Before continuing further, it is important to note that if the BoC had, as a result of its bond purchases, done nothing further and simply allowed a corresponding increase in bank reserves, the end effect would have been a flood of new reserves entering the banking system, significantly distorting the main trend-setting interest rate targeted by the BoC, called the “overnight rate”. Such a large increase in the supply of reserves would have caused a large reduction in the overnight rate, driving down the cost of loans to the general public along with all the inflationary implications this process would have entailed. Instead, in order to keep a lid on any potential inflationary problems that would almost certainly manifest itself down the road, the BoC engaged in a process economists call “sterilization” to counterbalance the increase in bank reserves resulting from their bond purchases.

To explain the process of sterilization further, as part of their regular debt-issuing process, the Federal Government sells securities (such as T-Bills) and deposits the proceeds of these transactions into accounts held at the various commercial banks. These accounts constitute deposit money of the Federal Government and are counted as part of the money supply since they are available for spending on various government programs and initiatives. When the BoC engaged in asset purchases in response to the 2008 crisis, it had the end effect of flooding the banking system with newly created bank reserves, but the inflationary effect of such large-scale money issuance was counterbalanced by removing Federal Government deposit money from the commercial banks and transferring it to Federal Government deposit money held at the BoC. The money created to fund the asset purchases was essentially moved into a black-hole at the BoC, with what can only be assumed to be a guarantee from the Federal Government that these funds would be held in reserve and not be spent into the broad economy.

We can further see that in August 2010, with the height of panic largely behind them and emergency liquidity measures no longer needed, the BoC subsequently unwound their emergency asset purchases, which is represented by the large reduction in the purple area on Chart 1. By selling its portfolio of securities and retiring the money proceeds from the public sphere, the deflationary aspect of the asset sales was similarly counteracted by releasing Federal Government deposits back into the public banking sector. This is represented by the large reduction in the green area in Chart 2. The net effect was that as a result of the BoC’s asset purchases and sales from 2008 to 2010, the amount of reserves held in the banking system remained largely consistent, reflected by the fact that “Bank Deposits” remained relatively stable over the entire time-period covered in Chart 2.

But if no new money was released into the economy as an end result of the BoC bond purchases during the Great Recession, what then was the whole point of the supposed “debt monetization” pursued by the BoC during the 2008 crisis? It turns out that monetizing debt, in the strict sense of the word, was not in fact the primary objective of the unprecedented expansion of the BoC balance sheet during the time of the 2008 financial crisis. Rather, it seems that there was a much greater emphasis placed on propping up asset prices in order to maintain low lending rates than there was on providing monetary stimulus to the Canadian financial system.

The central bank response of large-scale bond purchases during the 2008 financial crisis, then, can be thought of less as “quantitative” easing per se, and more as a form of “qualitative” easing. The BoC responded to the crisis by altering the composition of its balance sheet without actually liquefying the economy. It accepted lower quality bond securities onto the asset-side of its balance sheet to drive down borrowing costs, add liquidity to debt markets, and, one can only assume, to prevent a widespread fire-sale of these same securities. Because the BoC “money-printing” never in fact flowed into the public domain, it is not technically correct to label the BoC emergency response as asset monetization in the strict sense of the word. In order for the operation to be labelled as “QE”, the Federal Government would have been required to spend its deposits held at the BoC into the broad economy which would have had an upwards influence on general prices and served to counteract the natural deflationary effect triggered by the 2008 financial crisis.

It is of course important to remember that at the time that all of this was happening, there were real worries that the Federal Government would in fact attempt to finance budget deficits and stimulus spending with their deposits held at the BoC. In fact, there were certainly people in some quarters arguing that the asset purchases should not be sterilized, and that with the bigger worry at the time being deflation, newly created BoC money should indeed be permitted to increase reserve balances in a bid to prop up general prices and stoke higher inflation expectations. In hindsight it is obvious that such actions would likely have proven to be largely overkill, but readers should recognize that this is indeed another bullet in the government’s arsenal which, while never fired, remains a real and tangible tool available during future emergency asset monetization programs in times of crisis. We have simply never used it here in Canada to date.

Having now covered the BoC policy response to the financial crisis of 2008, the second part of this series will cover the current state of the BoC balance sheet, the suite of tools currently available to the BoC and the Federal government to respond to future emergencies, and probable policy responses to the coming liquidity and solvency crisis of which the Canadian housing market will likely be the major epicenter.

Note: A previous version of this article failed to explain that new money created by the BoC to fund asset purchases was added via the addition of commercial bank reserves, and not deposit money held at the banks. This has since been corrected.